Four Companies Redefining What Space Is For - From Reusable Rockets to Orbital Factories

1. Background: Space Goes Mainstream

The space economy is rapidly becoming a core pillar of the global economy. In 2024, it reached roughly $613 billion, continuing a steady ~7% annual growth trajectory. Looking ahead, most estimates place the market on a path toward $1 trillion in the early 2030s ($1.8 trillion by 2035 estimated by McKinsey) and much higher beyond that. Private capital is accelerating this shift: investment in space companies has surged in recent years, with 2026 already seeing record funding levels - nearly $8 billion raised in the first quarter alone.

Source: Reuters, Copyright © Jarsy Research

What is driving this surge? Three converging forces.

First, launch costs have fallen dramatically, thanks in large part to SpaceX’s reusable Falcon 9 and Falcon Heavy, the cost of sending payloads to low Earth orbit has dropped below $1,500 per kilogram, down from more than $10,000 (Falcon 1) 20 years ago. From 2022 to 2025, launch cadence has grown from more than 2 days to 27 hours / launch. (see below)

Source: SpaceX, planet4589.org. Copyright © Jarsy Research

Second, advances in satellite miniaturization and mass production have made space-based services economically viable, unlocking commercial applications from global broadband to real-time Earth observation. Third, a new generation of space stations, in-orbit manufacturing platforms, and even early-stage mining ventures is laying the foundation for a true orbital economy, one that extends far beyond simply launching and retrieving assets.

2. Four Emerging Frontiers

The most exciting companies in 2026 are no longer just asking how to reach space, but what to do once there. Several sectors are emerging in parallel, each moving toward commercial viability:

Commercial Space Stations: With the ISS expected to retire around 2030, successors are advancing quickly. Axiom Space has already flown private missions and is building modules that will evolve into a standalone station, while others like Orbital Reef (Blue Origin + Sierra Space) and Vast are developing alternative habitats.

Reusable Launch: First-stage reuse is proven; full reusability is next. Companies like Stoke Space, alongside Rocket Lab and Relativity Space, are pushing new systems, while SpaceX continues iterating toward full-stack reuse.

Satellite Connectivity: Connectivity is scaling across LEO and GEO. Starlink leads in LEO, with Amazon’s Kuiper (Now Amazon LEO) ramping up, while Astranis is rethinking GEO with smaller, faster-to-deploy satellites.

In-Space Manufacturing: Moving beyond experiments, companies like Varda are demonstrating the ability to manufacture in orbit and return products, with growing commercial and government interest.

Each frontier is being shaped by a new generation of companies. This research looks at four (one from each sector) and how they are turning early momentum into real capability.

3. Four Builders of the New Space Economy

a. Axiom Space: Building Humanity’s Next Home in Orbit

With the International Space Station expected to retire around the end of this decade, a commercial successor will be needed. Axiom Space is one of the leading contenders, and already one of the most active commercial operators of human spaceflight missions.

Founded in 2016 by Dr. Kam Ghaffarian (who previously built NASA’s second-largest engineering services contractor) and Michael Suffredini (NASA’s ISS Program Manager from 2005 to 2015), Axiom was built by people who literally ran the space station and understood exactly what its commercial successor would need.

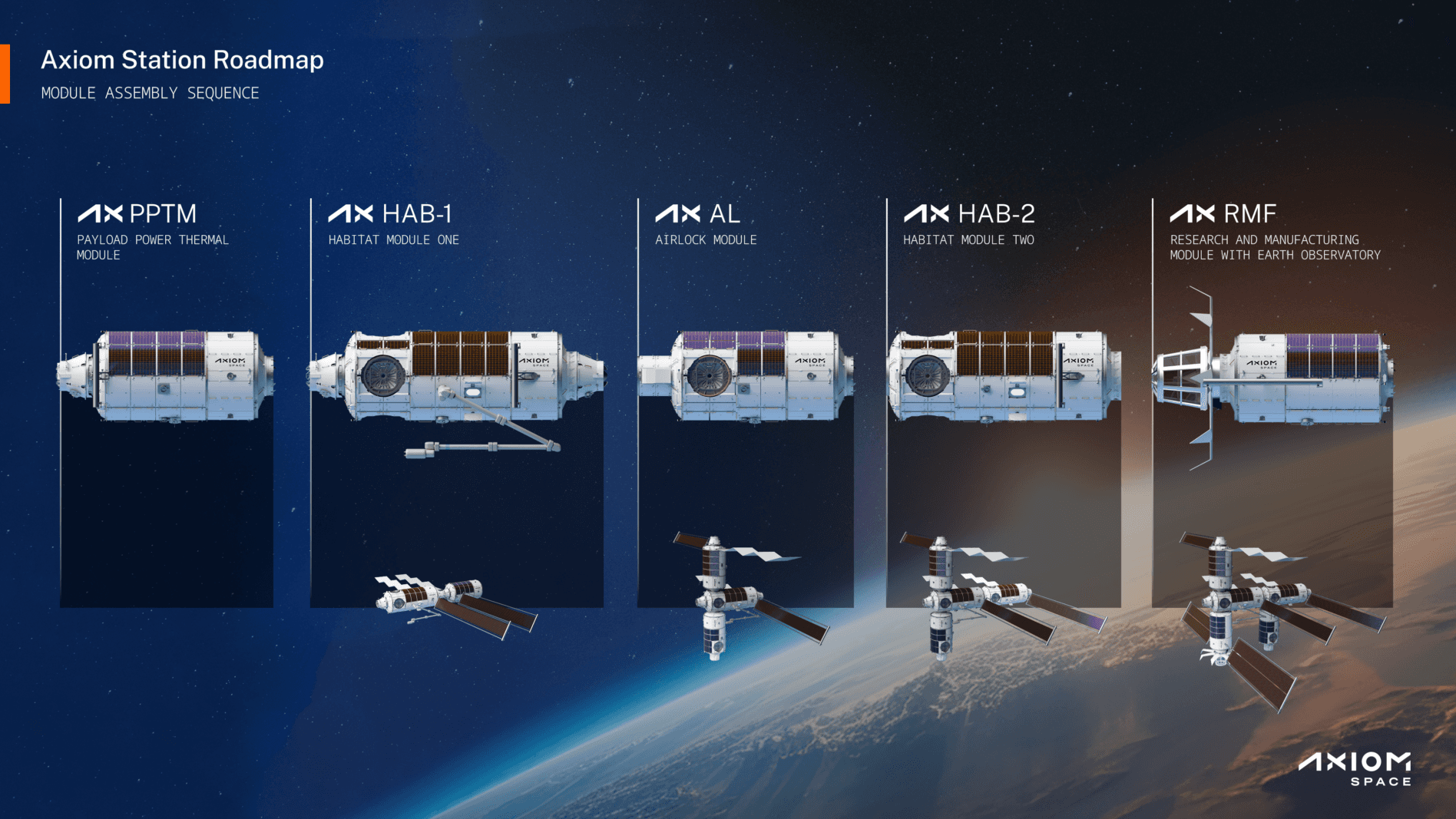

The Plan: Attach, Then Detach

Image Credit: Axiom Space

Axiom’s product, the Axiom Station, follows a modular architecture (~5 modules), starting with a Payload Power Thermo Module (PPTM) and Habitant Module (HAB-1). The first two modules are expected to form an initial independent station, with further expansion over time.

Their strategy is deliberately pragmatic. It plans to attach its first module PPTM to the ISS (targeting in 2027-2028) leveraging existing infrastructure while validating its own systems in orbit. Additional modules will follow and eventually detach into a free-flying station later in the decade. Manufacturing is already underway, with Thales Alenia Space producing primary structures.

Left: A digital rendering of the completed Axiom Station, which includes the Payload, Power, and Thermal Module, Habitat 1, an airlock, Habitat 2, and the Research and Manufacturing Facility. Rright: Axiom envisions their first module would be attached to the International Space Station's forward-most port. The commercial crew mating adapter (seen in black) currently on that port could be relocated to the top of the new module. Image Credits: Axiom Space

This contrasts with Vast, which is targeting a single-module Haven-1 launch in 2027, potentially reaching orbit first, but with a smaller, short-duration platform that relies heavily on SpaceX for critical systems. Axiom’s approach is slower, but reduces risk through incremental validation on the ISS.

Revenue Today, Station Tomorrow

While building its station, Axiom Space generates revenue through private astronaut missions to the International Space Station, flying crews on SpaceX’s Crew Dragon. It has also secured a NASA contract for next-generation spacesuits (AxEMU) and raised over $1 billion in funding. While newer entrants may reach orbit sooner, Axiom’s incremental approach is designed to deliver a more complete successor to the ISS.

2. Stoke Space - The Next Launch Revolution

SpaceX showed that reusing a rocket’s first stage can significantly reduce launch costs, but it has not yet achieved full reuse of an entire orbital rocket. Stoke Space, founded in 2019 by Andy Lapsa and Tom Feldman (both former Blue Origin engineers), is developing Nova, a fully reusable rocket designed from the outset to return both stages.

The Upper Stage Breakthrough

The hardest unsolved problem in rocketry is reusing the upper stage. It reaches orbital velocity - roughly 28,000 km/h - and must survive reentry temperatures exceeding ~1,500°C. SpaceX’s Starship uses ceramic heat shield tiles; Stoke has taken a different approach. The upper stage of Nova integrates a regeneratively cooled metallic heat shield with 24 rocket engine thrust chambers arranged in a ring around the base. This system, known as the Andromeda engine, combines propulsion and thermal protection into a single structure. During reentry, cryogenic hydrogen circulates through the vehicle to absorb heat, while the same propulsion system is used for the final descent and landing. This approach eliminates the need for fragile thermal tiles and is designed to enable rapid reuse with minimal refurbishment between flights. Nova targets ~3,000 kg to low Earth orbit in fully reusable mode.

(Left) Andromeda 1. (Right) Andromeda 2 (right) seen in its shipping fixture next to Zenith Engine (left, for 1st stage). Image Credits: Stoke Space

Backed by over $1B in funding and developing infrastructure at Cape Canaveral’s Launch Complex 14, the company is targeting initial orbital test flights no earlier than 2026, with commercial operations dependent on demonstrating reliable recovery and rapid reflight. The promise is a 20x reduction in cost to orbit compared to expendable vehicles.

3. Astranis - Reinventing GEO Satellites

Astranis was founded in 2015 by John Gedmark and Ryan McLinko (ex-Planet Labs), emerging from Y Combinator with a contrarian vision: instead of massive, billion-dollar geostationary satellites or large low-Earth orbit constellations, build small, dedicated satellites for high orbits.

Image Credits: Spacewatch.global

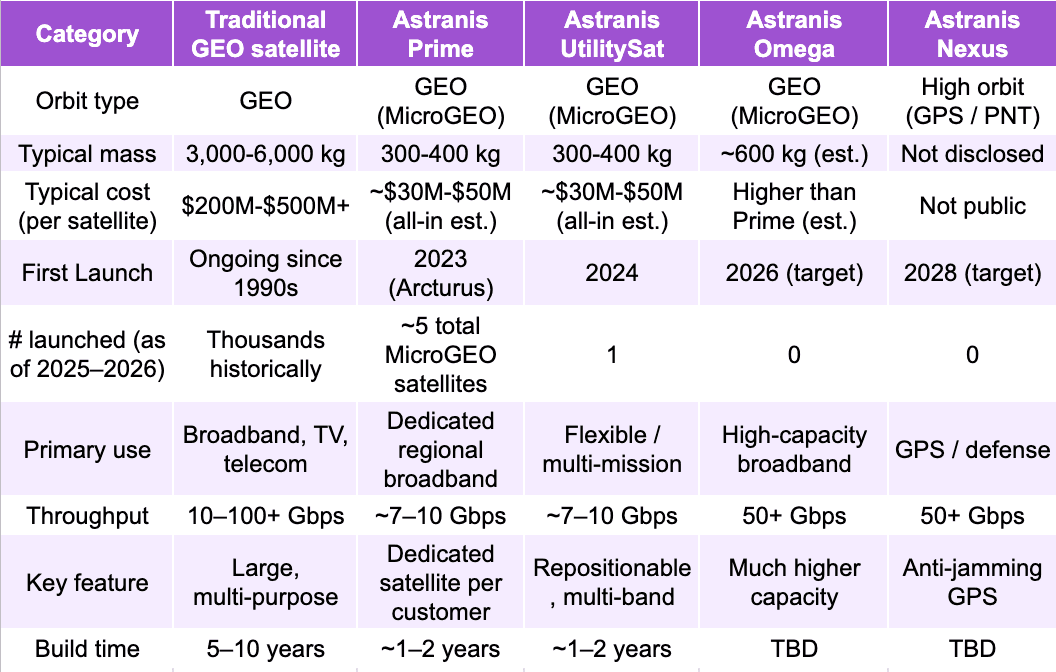

Its core product family: Prime, UtilitySat, Omega, and Nexus, is built on a shared MicroGEO platform, a dramatically smaller (~300-600 kg) satellite compared to traditional multi-ton GEO systems. The key technology is a software-defined radio (SDR) payload, which allows bandwidth, frequency, and coverage to be reconfigured in orbit, enabling both dedicated single-customer satellites and flexible, multi-mission spacecraft. While SDR itself is not new, Astranis’s advantage lies in integrating it into a low-cost, standardized GEO platform designed for rapid manufacturing and deployment, effectively turning satellites into reprogrammable infrastructure rather than fixed hardware.

Source: Astranis, Wikipedia. Copyright © Jarsy Research

Astranis has moved from prototype to early deployment, with its first commercial satellite launched in 2023 and additional satellites deployed in subsequent missions, while next-generation systems like Omega and Nexus are targeted for the mid-to-late 2020s. Its roadmap includes multi-satellite “Block” deployments through 2025 and beyond, with a long-term goal of launching and operating over 100 satellites by 2030. Backed by over $700M in funding and more than $1B in contracted revenue, the company is positioning itself as a hybrid between traditional GEO operators and LEO constellations, offering lower-cost, faster-deployed, and more flexible high-orbit connectivity.

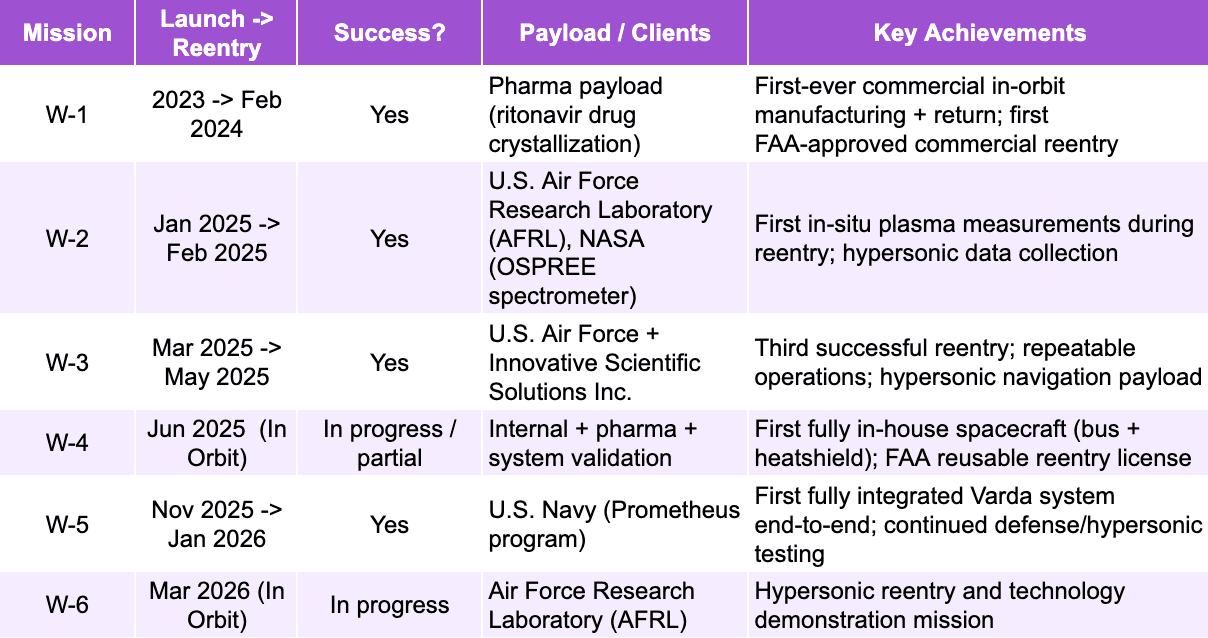

4. Varda Space Industries - Manufacturing in Microgravity

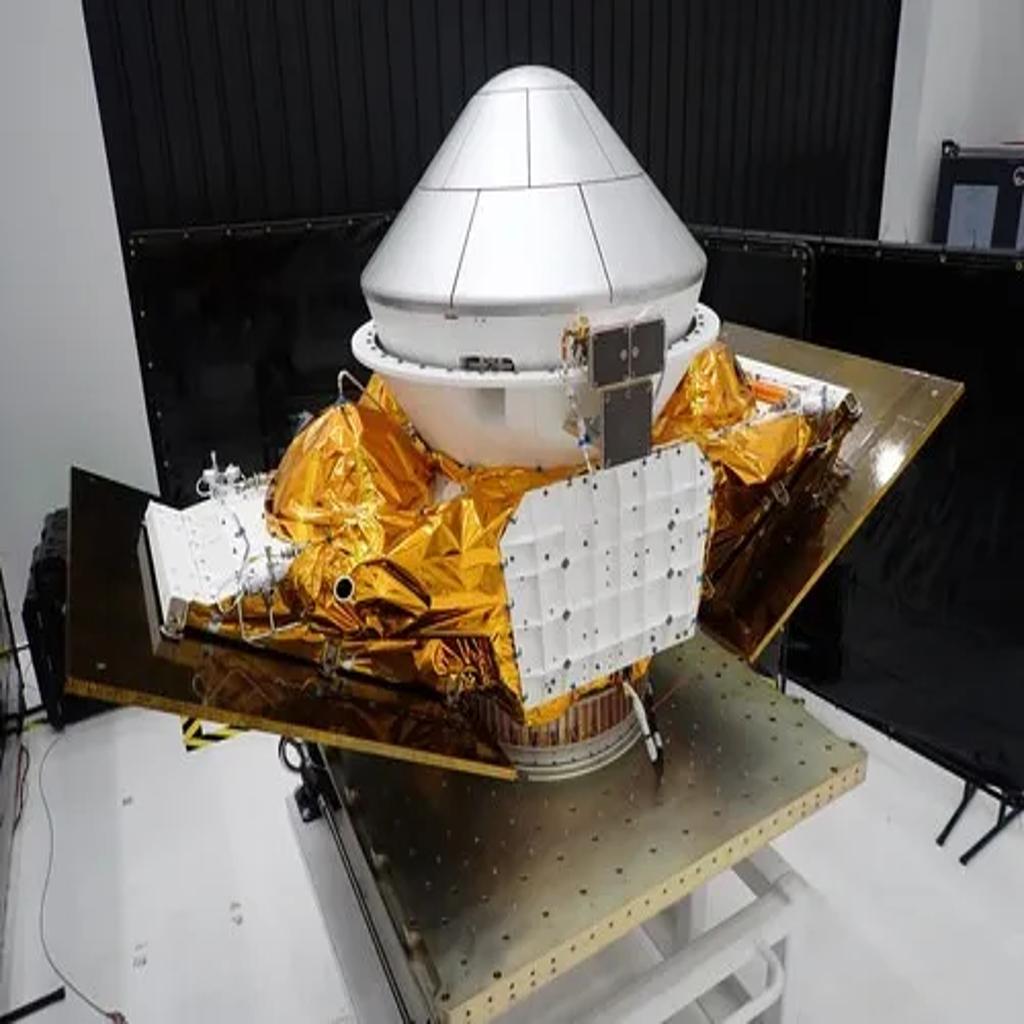

Varda Space Industries was founded in 2020 by Will Bruey (ex-SpaceX engineer), and Delian Asparouhov of Founders Fund, with a simple but ambitious idea: use space as a manufacturing environment and bring products back to Earth. Instead of launching satellites that remain in orbit, Varda builds spacecraft designed to operate in microgravity, produce high-value materials, and return them safely to the ground.

Varda’s system combines an orbital manufacturing platform with a reentry capsule, enabling end-to-end production in space. In microgravity, certain materials, particularly pharmaceutical crystals, can form with greater uniformity and fewer defects than on Earth. The company’s spacecraft hosts these processes in orbit, then returns the finished products using a heat-shielded capsule capable of surviving reentry at orbital velocities (~28,000 km/h). This integrated approach effectively turns space into a reprogrammable manufacturing environment, rather than just a location for experiments.

Left: W-4, Right: W-6 in a Falcon 9. Image Credits: Varda

W-Series missions so far:

Source: Varda. Copyright © Jarsy Research

Varda’s moat lies in the integration of microgravity manufacturing, spacecraft operations, and controlled reentry into a single system. While each component exists independently, few companies have demonstrated the ability to combine them into a repeatable pipeline. If successful, Varda could establish a new supply chain: manufacturing in orbit and returning goods to Earth, though it still must prove the economic viability and scalability of space-produced materials.

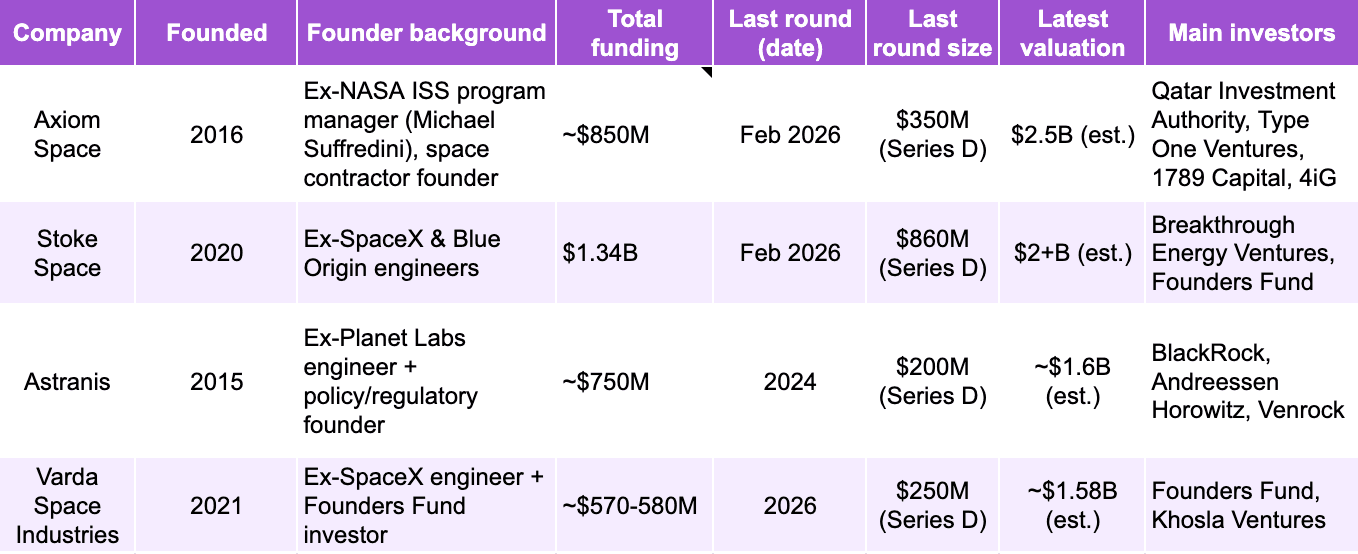

4. Funding and Outlook

Source: Stoke Space, Crunchbase, Pitchbook, Reuters, CNBC, ForgeGlobal.

Copyright © Jarsy Research

Across these startups, a new layer of the space economy is taking shape, each tackling a critical bottleneck with clear strengths and real risks. Stoke’s clean-sheet approach to full reusability is compelling, but it has yet to reach orbit. Astranis brings speed and cost efficiency to GEO, though it must prove reliability at scale. Varda has demonstrated the rare capability of routine reentry and early demand, but its long-term market is still uncertain. Axiom is advancing commercial space stations with strong partnerships, yet faces heavy capital and execution challenges. None of these bets are guaranteed, but together they signal a broader shift: space is moving from access to sustained, repeatable business, and for the first time, that future feels within reach. 🛰️🪐💫🚀🌌

Further Reading: Nasa Article on Axiom Space, Everyday Astronaut’s Video on Stoke Space, Astranis Avionics Systems, CNBC: The Space Manufacturing Race