From Sputnik to Starlink: a comprehensive guide to satellite history and technology, orbital mechanics, the modern competitive landscape, and the venture-backed companies reshaping the orbital economy. © 2026 Jarsy Research

1. A Brief History of Satellites

The word "satellite" comes from the Latin "satelles," meaning attendant or guard. In astronomy, it originally described natural moons orbiting planets. Today it refers to any object, natural or artificial, in orbit around a larger body. The story of artificial satellites spans less than 70 years, but it has fundamentally changed how humanity communicates, navigates, observes the Earth, and projects military power.

1.1 The Space Race Era (1957–1969)

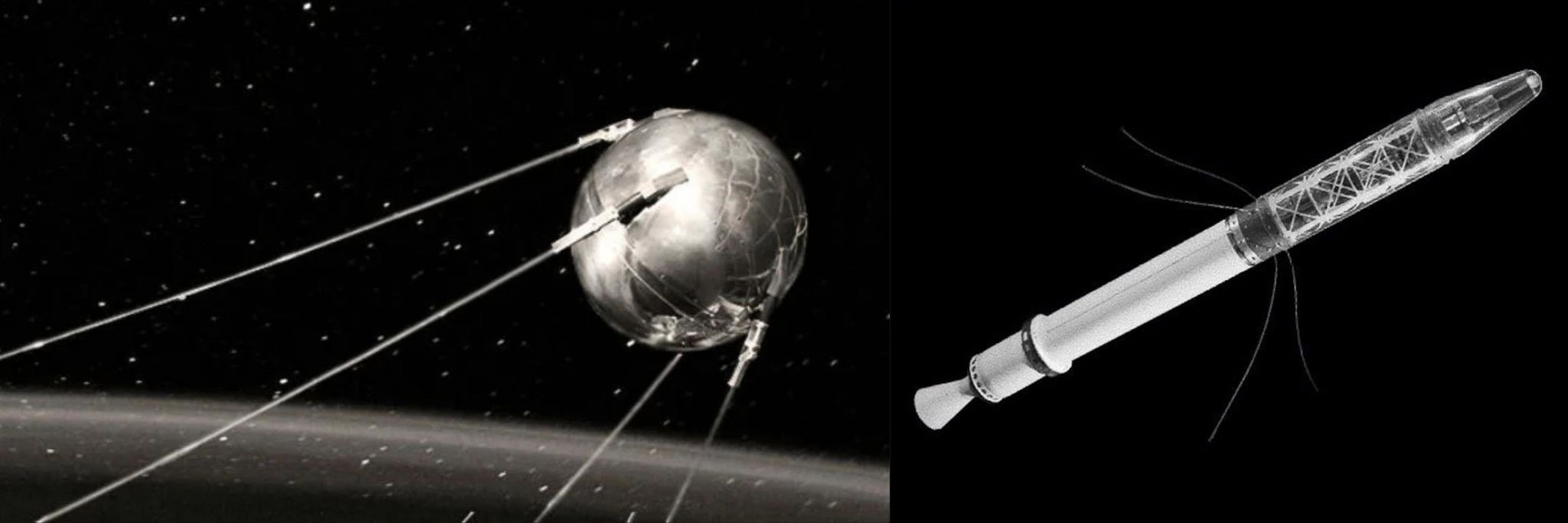

On October 4, 1957, the Soviet Union launched Sputnik 1, an 83 kg aluminum sphere with four trailing antennas, into low Earth orbit. It did nothing except transmit a radio beep for 21 days, but it changed the world. Sputnik proved that objects could be placed in orbit, and it shocked the United States into creating NASA (1958) and pouring resources into space.

The U.S. responded quickly. Explorer 1 launched in January 1958 and discovered the Van Allen radiation belts. In 1958, the U.S. also launched SCORE, the first communication satellite, which broadcast a pre-recorded Christmas message from President Eisenhower, the first time a human voice was transmitted from space.

Sputnik 1 (left) and Explorer 1 (right). Image Credits: Discovery.com, NASA

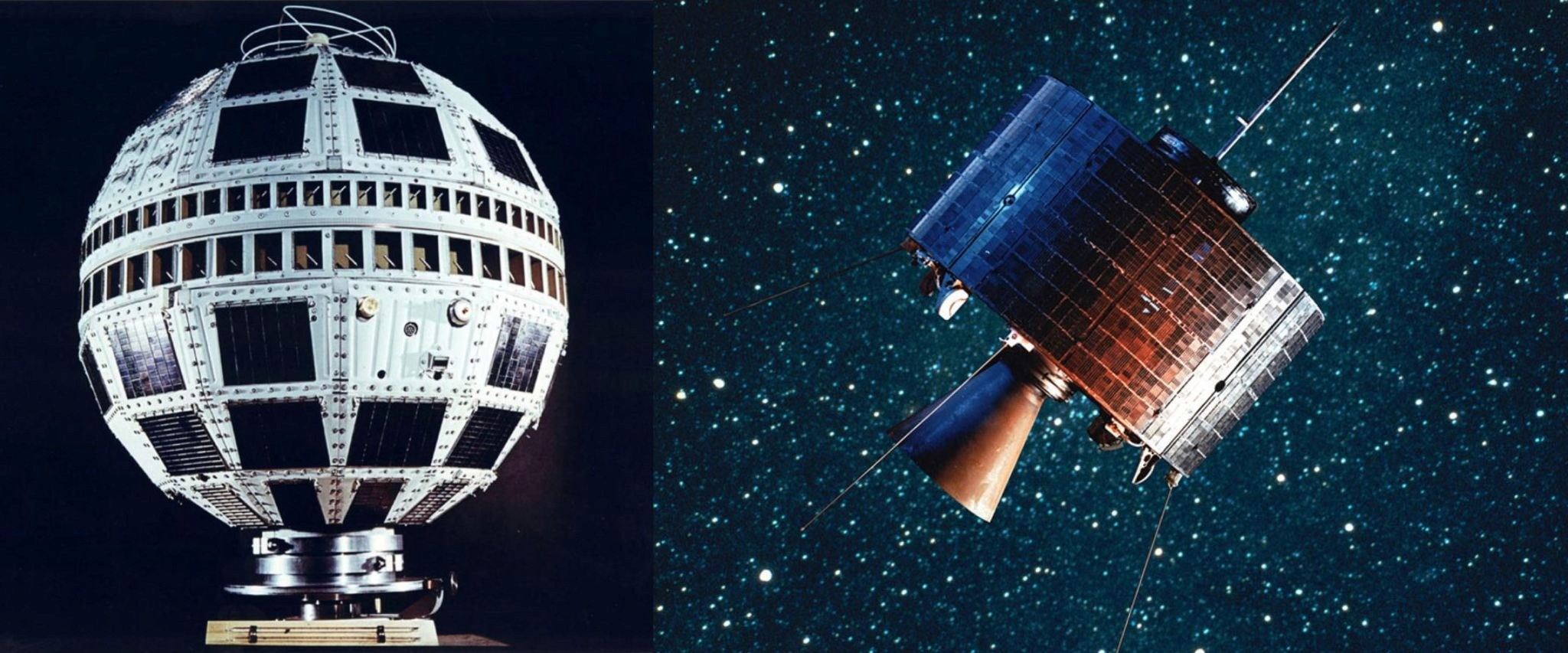

The early 1960s saw rapid advances in satellite communication. Echo 1 (1960), a giant metallic balloon built by NASA, acted as a passive signal reflector, while Telstar 1 (1962), built by Bell Labs for AT&T, became the first active communication satellite and carried the first live transatlantic TV broadcast. The major breakthrough came with Syncom 2 and Syncom 3 (1963-1964), built by Hughes Aircraft Company, which were the first geostationary satellites. Orbiting 35,786 km above Earth, they appeared fixed in the sky, enabling continuous communication links. Syncom 3 broadcast the 1964 Tokyo Olympics worldwide, proving the concept of permanent global satellite communication.

Telstar 1 (left) and Syncom 3 (right). Image Credits: Discovery.com, Boeing

In 1965, Intelsat (led by the United States) launched Early Bird (Intelsat I), the first commercial communication satellite. It could carry 240 telephone calls or one TV channel across the Atlantic. The satellite era of global telecommunications had begun.

1.2 The Commercial Era (1970s-2000s)

Through the 1970s and 1980s, GEO communication satellites became the backbone of global telecommunications, carrying telephone calls, television broadcasts, and data between continents. Intelsat grew into a global cooperative, operating dozens of GEO satellites.

Meanwhile, governments pursued navigation. The U.S. military's Transit system (1960s-1990s) was the first satellite navigation system, used to track nuclear submarines. In 1978, the first GPS satellite (NAVSTAR) launched, beginning what would become the most consequential satellite program in history. GPS reached full operational capability in 1995 with 24 satellites in MEO. Russia's GLONASS followed a similar timeline.

NAVSTAR (left) and Iridium Satellite (right). Image Credits: wikipedia.org

Earth observation also matured. Landsat 1 launched in 1972, beginning the longest continuous record of Earth's surface from space. Weather satellites (TIROS, NOAA series) became essential for forecasting. Military spy satellites (classified programs like CORONA, KH-11) provided strategic intelligence throughout the Cold War.

The 1990s brought the first attempt at a LEO communication constellation: Iridium. Motorola conceived a 66-satellite network for global mobile phone service, an audacious idea that launched in 1998 at a cost of $5 billion, attracted only 10,000 subscribers (the handsets cost $3,000 each), and filed for bankruptcy in 1999. It was later acquired for $25 million and rebuilt as a niche provider for maritime, aviation, and military users. Iridium's failure was a cautionary tale that haunted the industry for two decades, until SpaceX's Starlink proved LEO broadband could work at scale.

1.3 The New Space Era (2010s-Present)

Starting around 2010, a convergence of cheaper launches, miniaturized electronics, and venture capital created what the industry calls "New Space." Planet Labs (founded 2010) showed that fleets of cheap, small satellites could outperform a few expensive ones. SpaceX drove launch costs down by 10x. CubeSats (standardized 10×10×30 cm satellite modules), made orbit accessible to universities and startups for the first time.

The result has been explosive growth. As of 2026, there are over 15,000 active satellites in orbit, more than quadruple the number in 2019. SpaceX's Starlink alone accounts for over 10,000 of them. The satellite industry generates approximately $400 billion in annual revenue (2026), with communication services representing the largest segment.

Planet Labs Dove 1 (left) and Starlink v1 (right). Image Credits: US National Air and Space Museum, SpaceX

2. Understanding Satellite Orbits

A satellite stays in orbit because its forward velocity balances Earth's gravity. It is constantly falling toward Earth, but moving sideways fast enough that it keeps missing the ground. The higher the orbit, the weaker gravity becomes and the slower the satellite needs to travel. This relationship, described by Newton's law of gravity and Kepler's laws of motion, determines how different orbits are used.

The orbital velocity of a satellite at altitude h is:

v = √(GM / (R + h))

where G is the gravitational constant, M is Earth's mass, and R is Earth's radius. At 550 km altitude (the orbit used by Starlink satellites), a spacecraft travels at roughly 7.6 km/s and completes an orbit every 96 minutes, circling Earth about 15 times per day.

As altitude increases, orbital speed decreases but orbital period increases. At 35,786 km, the altitude of geostationary orbit (GEO), a satellite travels at about 3.07 km/s and takes 23 hours 56 minutes to complete one orbit. Because this matches Earth's rotation, the satellite appears fixed above the same point on the surface, making GEO ideal for communications and weather monitoring.

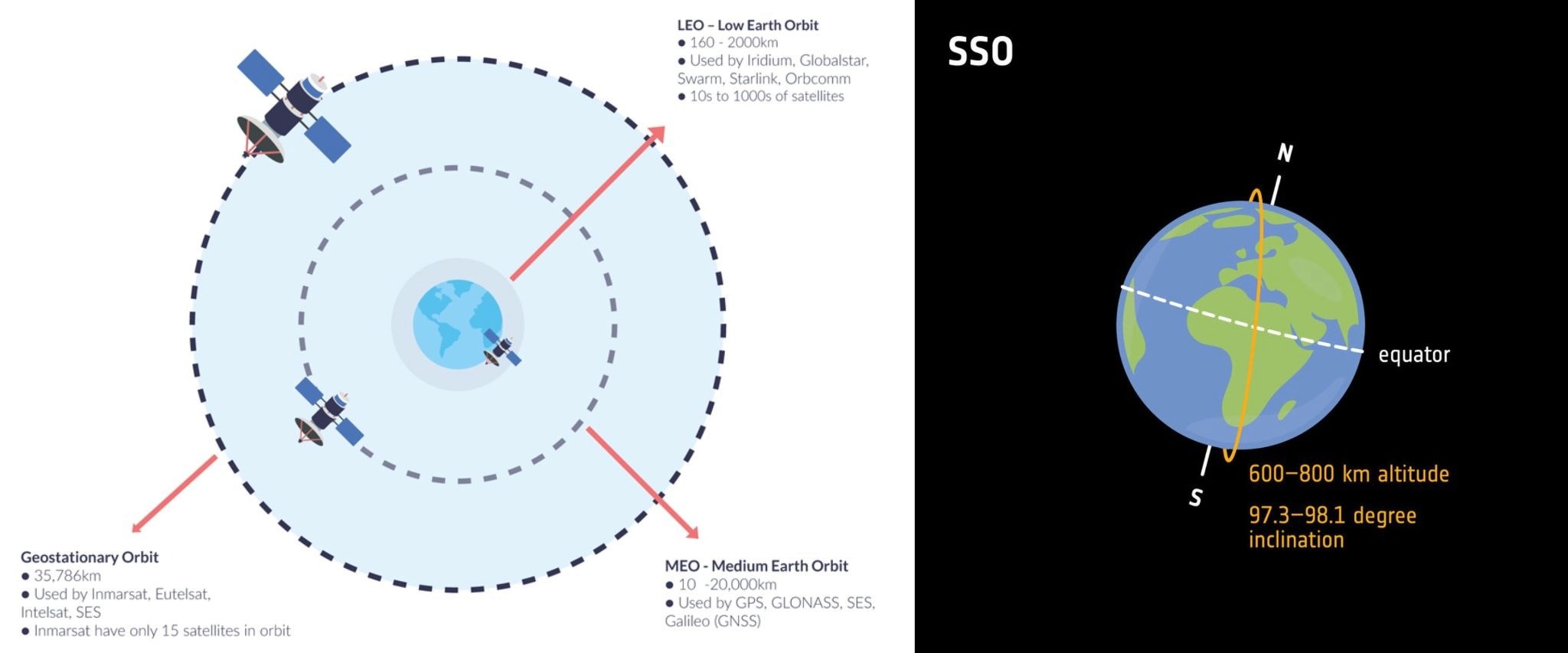

Major Satellite Orbits

Satellite orbits are defined by altitude and geometry, each involving trade-offs between coverage, latency, launch cost, and the number of satellites required.

LEO/MEO/GEO (Left) + SSO (Right). Image Credits: groundcontrol.com, The European Space Agency

Low Earth Orbit (LEO) is the closest and most active orbital regime. Its proximity to Earth enables low-latency communications and high-resolution imaging, making it the preferred choice for broadband networks and Earth observation. The trade-off is limited coverage per satellite, requiring large constellations to achieve global service. Companies such as SpaceX, OneWeb, Amazon Leo (Project Kuiper), and Planet Labs operate in LEO.

Geostationary Orbit (GEO) is a unique orbit where a satellite's orbital period matches Earth's rotation, causing it to appear fixed above a single point on the equator. This allows continuous coverage of large regions and simplifies ground infrastructure, making GEO the traditional choice for television broadcasting, communications, and weather monitoring. Major operators include Intelsat, Eutelsat, and Inmarsat.

Medium Earth Orbit (MEO) occupies the space between LEO and GEO. Satellites in MEO cover much larger areas than those in LEO while maintaining lower latency than GEO, making the orbit particularly well suited for global navigation systems. GPS, Galileo, GLONASS, and BeiDou all operate primarily in MEO.

Sun-Synchronous Orbit (SSO) is a specialized near-polar orbit within Low Earth Orbit (typically 500-900 km altitude, but mainly 600-800 km altitude). By passing over locations at roughly the same local solar time on each orbit, SSO provides consistent lighting conditions that make images easier to compare over time. As a result, it is widely used for mapping, environmental monitoring, agriculture, and reconnaissance. Operators such as Planet Labs, Maxar, and ICEYE rely heavily on SSO.

Orbits Comparison. Sources: Wikipedia, gogoair.com. © 2026 Jarsy Research

3. The Modern Satellite Landscape

The satellite industry is the largest segment of the global space economy. According to the Satellite Industry Association (SIA) and BryceTech, satellite-related revenues reached approximately $303 billion in 2025, accounting for roughly 71% of the $429 billion global space economy.

The industry can be broadly divided into four major segments: communications, Earth observation, navigation, and emerging space services.

3.1 Communications & Broadband

Communications remains the largest satellite market. LEO constellations such as Starlink, Kuiper, and OneWeb provide low-latency global connectivity, while GEO operators including SES, Eutelsat, Intelsat, and Viasat continue to dominate broadcasting and regional communications. A rapidly emerging category is direct-to-device connectivity, led by AST SpaceMobile and Starlink.

3.2 Earth Observation & Remote Sensing

Earth observation satellites collect data using optical cameras, synthetic aperture radar (SAR), and radio-frequency sensors. Leading operators include Planet Labs and Maxar (optical imaging), ICEYE and Capella Space (SAR), and HawkEye 360. Increasingly, the value lies not in imagery itself but in AI-powered analytics and intelligence products.

ICEYE Satellites. Image Credit: ICEYE.com

3.3 Navigation

Global navigation systems such as GPS, Galileo, GLONASS, and BeiDou provide positioning, navigation, and timing services that underpin modern transportation, telecommunications, finance, logistics, and military operations. Though government-funded, they support trillions of dollars in economic activity worldwide.

3.4 Defense & National Security

Defense has become a major customer across nearly every segment of the satellite industry. Communications, Earth observation, navigation, and signals intelligence increasingly rely on commercial satellite infrastructure, making national security one of the strongest drivers of industry growth.

3.5 Emerging Space Services

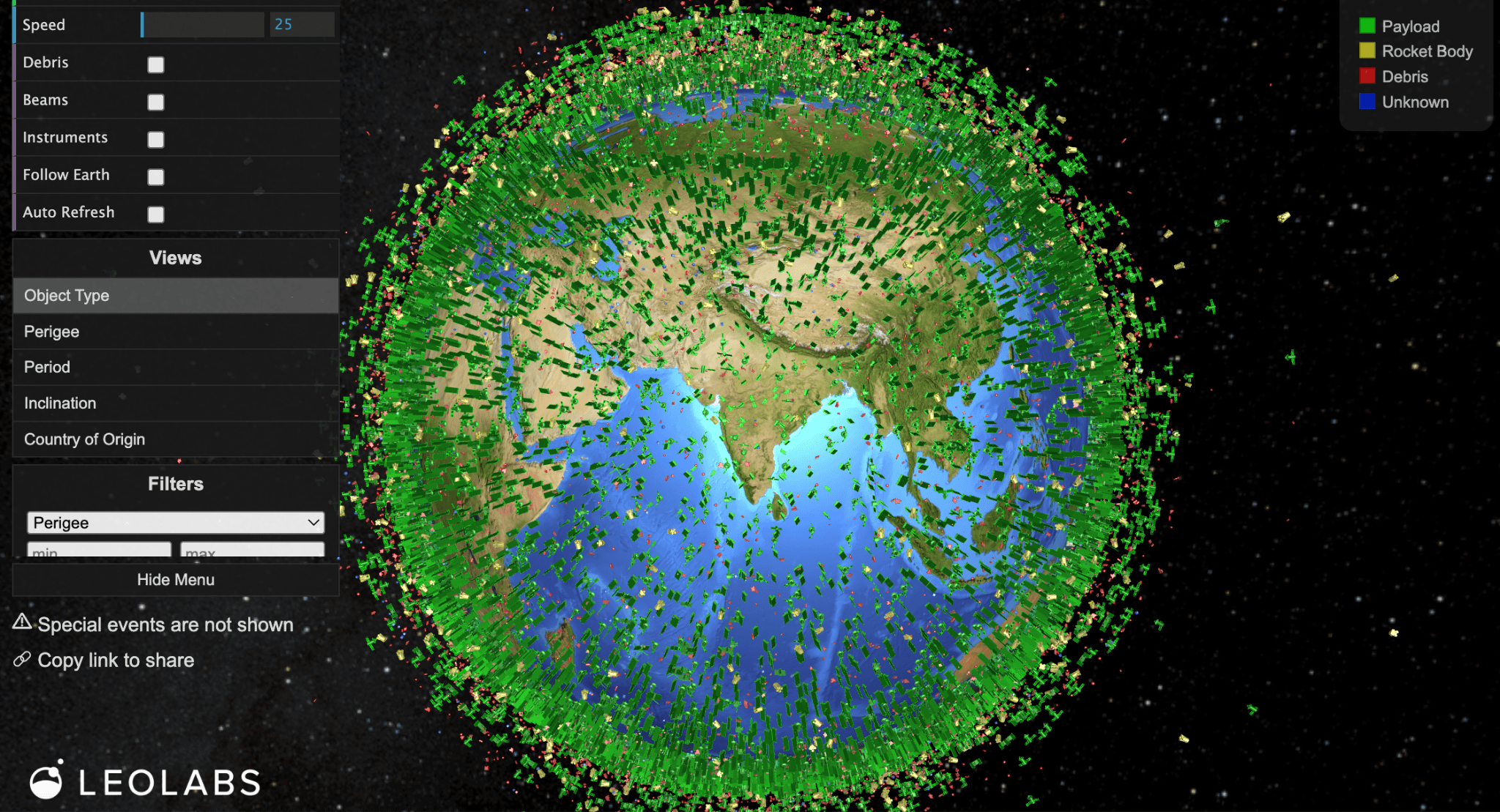

Several new categories are beginning to emerge beyond traditional communications, observation, and navigation. Space-based computing envisions AI training and inference in orbit, with startups such as Starcloud and SpaceX and research initiatives like Google's Project Suncatcher exploring orbital compute infrastructure (refer to Jarsy Research #18). On-orbit servicing, including satellite refueling, repair, life-extension, and debris removal, is being pioneered by companies such as Starfish Space, Astroscale, and Orbit Fab. Another emerging category is space situational awareness (SSA), where companies such as LeoLabs and Slingshot Aerospace track satellites and debris to improve orbital safety and traffic management.

Leolabs LEO Visualization. Image Credit: Leolabs

4. Technology Bottlenecks & Breakthroughs

Building and operating satellite constellations involves hard engineering constraints that limit what is possible at any given time. Below are the most important technical challenges facing the industry today, and the breakthroughs that are changing the equation.

4.1 Launch Cost (Breaking)

For decades, the single largest constraint on the satellite industry was the cost of reaching orbit. At $10,000-20,000/kg (pre-SpaceX era), only governments and large telecom operators could afford to launch. SpaceX's Falcon 9 brought this to ~$1,110/kg (estimated internal cost). Starship targets sub-$200/kg with full reusability and 100-150 (up to 200) tonne payload. At these prices, the economics of satellite constellations change fundamentally, it becomes cheaper to launch more satellites rather than build fewer, more capable (and more expensive) ones. See our previous report: "SpaceX’s Road to Sub-$200/kg".

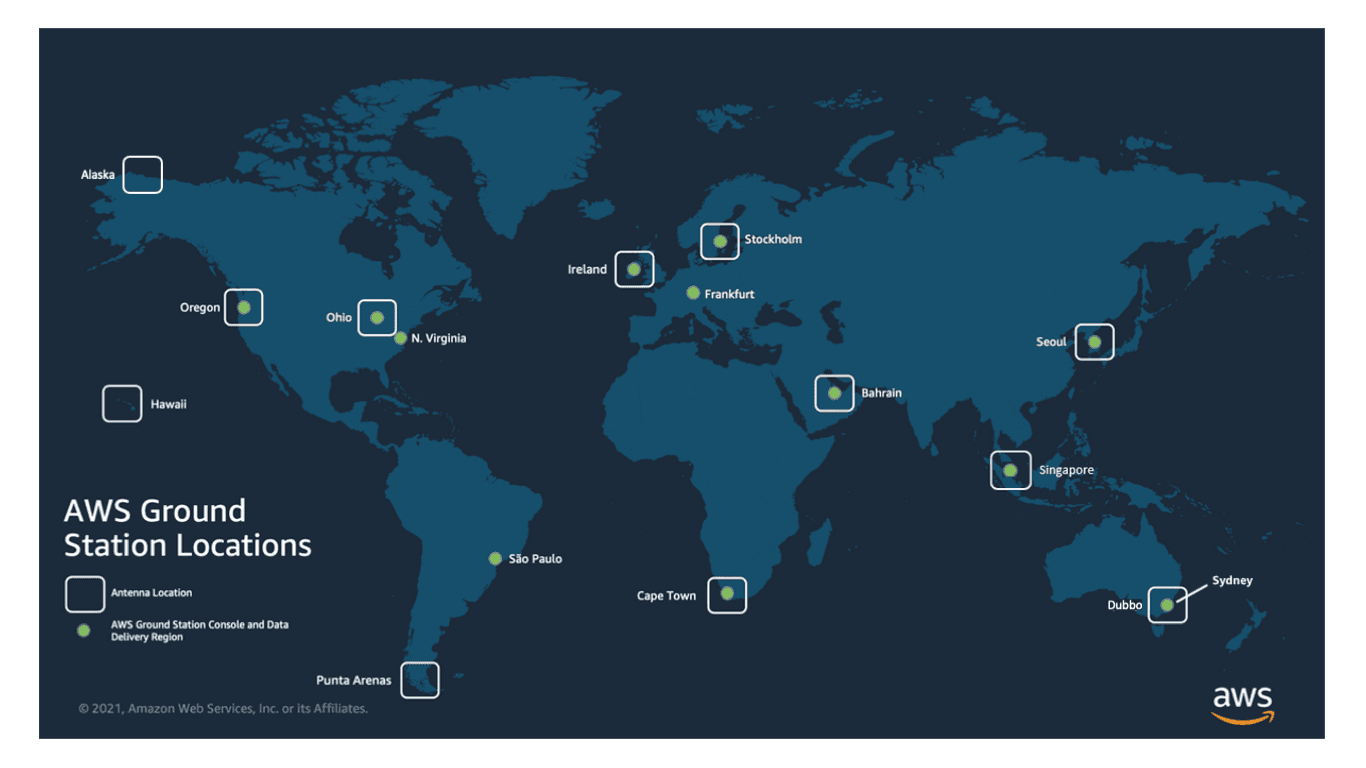

4.2 The Downlink Bottleneck (Active)

Satellites can collect far more data than they can send to the ground. A high-resolution imaging satellite may generate terabytes of data per day but only have limited opportunities to communicate with ground stations during each orbit. This "downlink bottleneck" is one of the primary constraints on space-based data services. Solutions include on-board AI processing (Planet, BlackSky, HawkEye 360), optical inter-satellite links (OISLs) (Starlink, Kuiper, Telesat Lightspeed), and expanding ground station networks (AWS Ground Station, Azure Orbital, KSAT). Together, these technologies reduce the need to transmit raw data and increase the effective capacity of satellite constellations.

OISLs illustrated by ETH Zurich. Image Credit: ETH Zurich

AWS Ground Stations. Image Credit: AWS

4.3 Software-Defined Satellites (Breakthrough)

Traditionally, a satellite's mission was fixed at launch: its transponders, frequencies, and coverage patterns were hardwired. Modern satellites are increasingly "software-defined," meaning their payload can be reconfigured in orbit. Beam patterns, bandwidth allocation, frequency assignments, and even mission type can be changed via software upload. This allows operators to respond to shifting demand without launching new hardware. SES's O3b mPOWER, Eutelsat's next-gen OneWeb, and several GEO platforms now use software-defined payloads.

4.4 Electric Propulsion (Maturing)

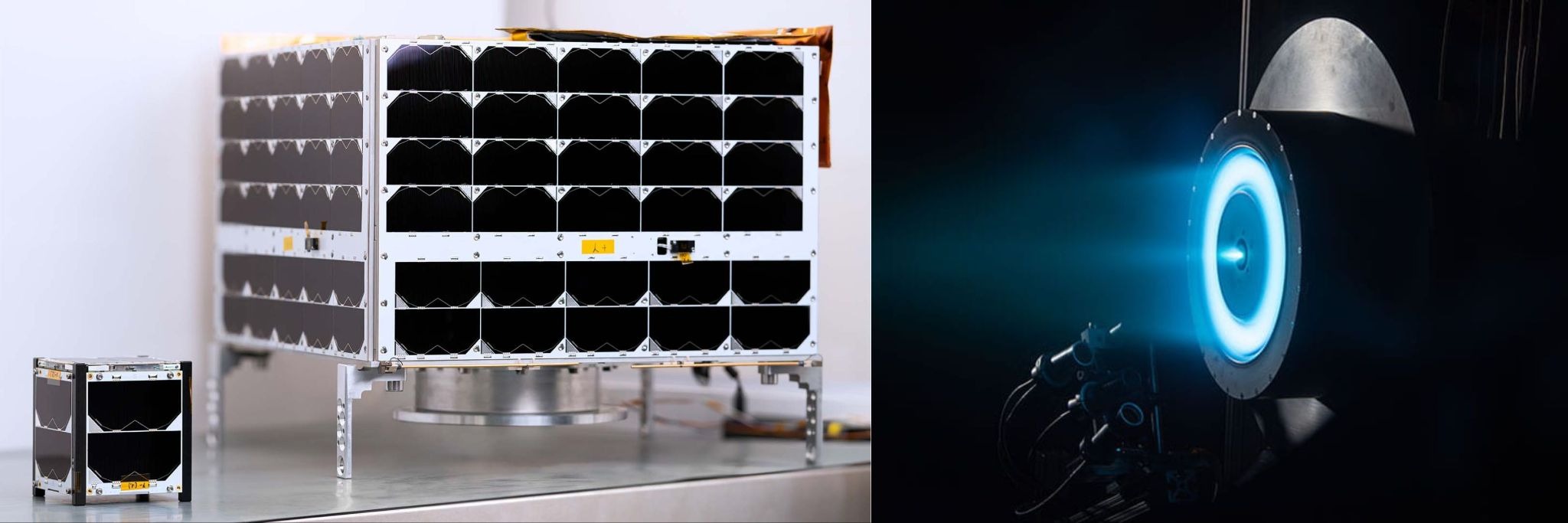

Chemical rockets are powerful but fuel-hungry. Electric propulsion (ion thrusters, Hall-effect thrusters) provides much higher fuel efficiency than traditional chemical propulsion, allowing satellites to carry less fuel and more payload. Electric propulsion is now standard for station-keeping in GEO (extending satellite life by years), orbit-raising for LEO constellations (Starlink uses krypton Hall thrusters), and even enabling very-low-Earth-orbit (VLEO) missions below 300 km, where continuous thrusting counteracts atmospheric drag for sharper imaging.

Nanoavionics CubeSats (left) and Hall Thruster (right). Image Credits: Nanoavionics.com, MIT, NASA

4.5 Miniaturization & Mass Production (Breakthrough)

Advances in electronics and manufacturing have dramatically reduced the size and cost of satellites. CubeSat and SmallSat platforms have enabled companies such as Planet, Spire, HawkEye 360, and ICEYE to deploy large constellations at a fraction of the cost of traditional spacecraft. In many applications, numerous smaller satellites can provide better coverage, revisit rates, and resilience than a handful of larger systems.

4.6 Thermal Management (Hard Problem)

In space, there is no air for convective cooling. Heat generated by onboard electronics must ultimately be rejected through thermal radiation, limiting how much computing power a satellite can carry. As satellites perform increasingly sophisticated onboard processing, thermal management is becoming a critical constraint. Scaling future applications such as orbital AI infrastructure will require more efficient processors, improved thermal architectures, or both.

4.7 Space Debris (Growing Risk)

The rapid growth of satellite constellations has increased the risk of collisions and orbital debris. Mitigation efforts include stricter deorbiting rules, debris removal missions by Astroscale and Starfish Space, and improved space situational awareness from companies such as LeoLabs.

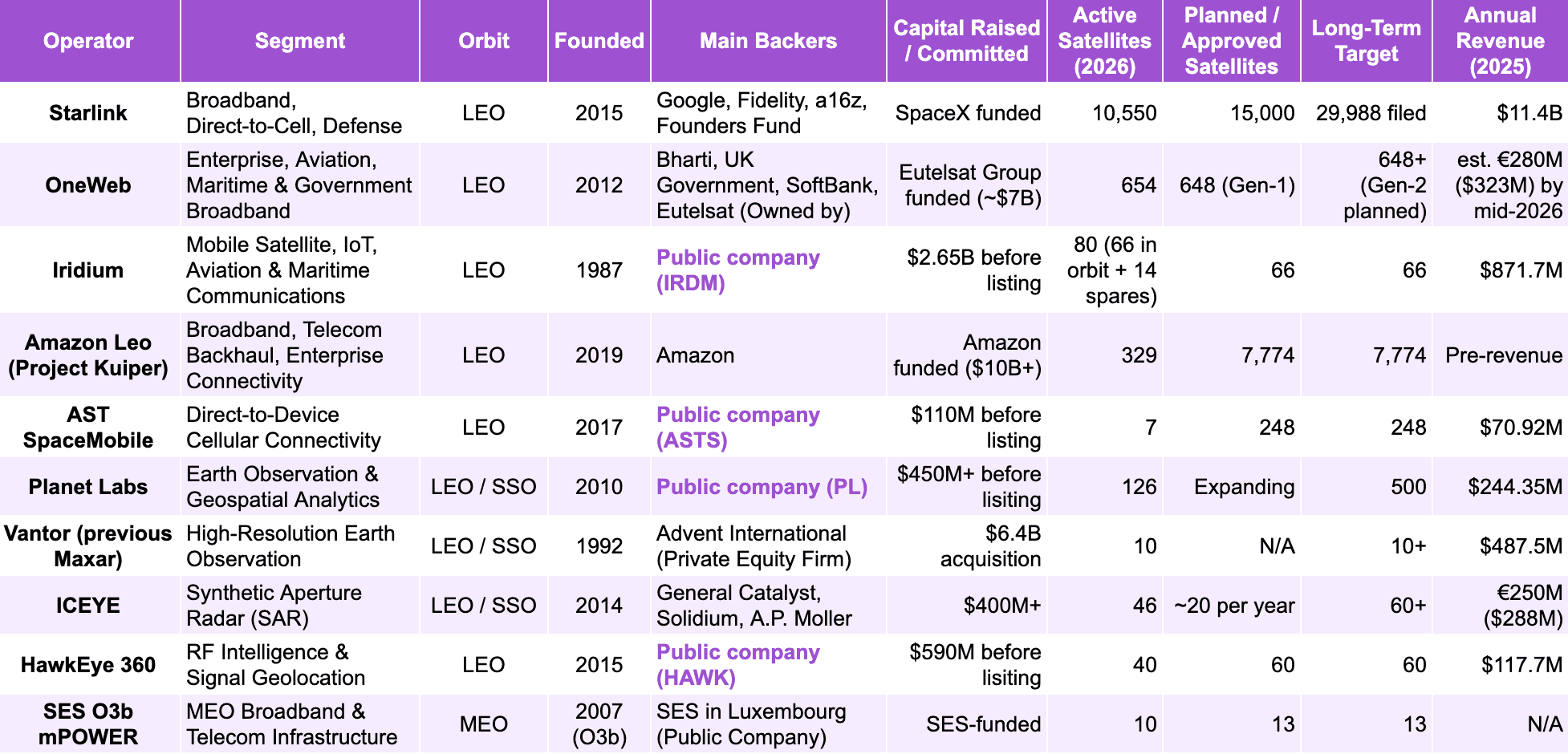

5. The Commercial and Venture-Backed Satellite Revolution

As discussed in Chapter 4, many of the technological bottlenecks that historically constrained the satellite industry are now being overcome. Lower launch costs, satellite miniaturization, and advances in computing and communications have dramatically improved the economics of operating in space. As a result, a new generation of venture-backed companies has emerged, building broadband networks, Earth observation constellations, and intelligence platforms that would have been impractical or uneconomic just a decade ago.

5.1 Leading Connectivity Networks

Starlink

Starlink was founded by SpaceX in 2015 as part of a broader vision to generate cash flow for Mars exploration. transformed the satellite industry by proving that a massive LEO broadband constellation could be commercially viable. Beyond residential broadband, the network now serves aviation, maritime, enterprise, government, and military customers, while also expanding into direct-to-cell services and the Starshield defense platform. Some industry observers view Starlink as a potential foundation for future space-based computing networks, given its scale, optical inter-satellite links, and close relationship with SpaceX's rapidly falling launch costs. (check our earlier research SpaceX 2.0)

Starlink v1 & v2. Image Credit: SpaceX

Iridium

Originally founded in 1987 by Motorola engineers seeking to create a truly global mobile communications network. Iridium's key advantage is truly global coverage, including the polar regions, through a constellation of 80 cross-linked satellites. Rather than competing in consumer broadband, Iridium focuses on aviation, maritime, defense, emergency communications, and IoT connectivity. Its Iridium NEXT constellation and globally licensed L-band spectrum create significant barriers to entry.

Amazon Leo (Project Kuiper)

Project Kuiper was launched in 2019 within Amazon. It is Starlink's most formidable challenger. Its key differentiator is integration with Amazon's broader ecosystem, particularly AWS cloud services and enterprise customers. With approval for 7,774 satellites and more than $10 billion committed, Amazon Leo aims to combine global connectivity with cloud computing and telecom infrastructure.

AST SpaceMobile

AST SpaceMobile was founded in the United States in 2017 by satellite entrepreneur Abel Avellan. The company is building a direct-to-device network that connects ordinary smartphones to satellites using existing cellular spectrum. Its BlueBird satellites deploy massive phased-array antennas and operate through partnerships with carriers including AT&T, Vodafone, Verizon, and Rakuten. AST has launched its first 7 satellites and received FCC approval for a 248-satellite constellation. If successful, it could significantly expand mobile coverage across the globe.

Image Credit: AST SpaceMobile

OneWeb

OneWeb was founded in the US in 2012 by satellite entrepreneur Greg Wyler, who previously founded O3b Networks. OneWeb pioneered the modern LEO broadband model and today operates a completed constellation of 648 satellites. Unlike Starlink's consumer focus, OneWeb primarily serves governments, defense agencies, airlines, maritime operators, and telecom providers. After a high-profile bankruptcy in 2020, the company was rescued by the UK Government and Bharti before merging with Eutelsat. Today, it represents Europe's largest operational LEO broadband network and one of the few global competitors to Starlink.

OneWeb satellites (left), Pelican Planet Labs (right). Image Credits: OneWeb, Planet Labs

5.2 Earth Observation & Intelligence

Planet Labs

Planet was founded in California in 2010 by former NASA scientists Will Marshall, Robbie Schingler, and Chris Boshuizen. The company pioneered the use of large numbers of inexpensive satellites rather than a small number of expensive spacecraft. Today, Planet operates the world's largest commercial Earth observation fleet, imaging nearly all of Earth's landmass every day and generating more than $300 million in annual revenue.

Vantor (previous Maxar)

Vantor traces its roots to DigitalGlobe, founded in the United States in 1992. The company became the gold standard for commercial satellite imagery, supplying the U.S. National Geospatial-Intelligence Agency and allied governments for more than two decades. Its WorldView and Legion satellites provide some of the highest-resolution commercial imagery available, with resolutions reaching approximately 30 centimeters.

ICEYE

ICEYE was founded in Finland in 2014 by Aalto University researchers Rafal Modrzewski and Pekka Laurila. The company pioneered synthetic aperture radar (SAR) microsatellites and has built the world's largest commercial SAR constellation, with more than 70 satellites (including decayed) launched. Unlike optical satellites, SAR can image through clouds, smoke, and darkness, making it valuable for defense, disaster response, and maritime monitoring. ICEYE surpassed €250 million in revenue in 2025, making it one of Europe's leading NewSpace companies.

HawkEye 360

Founded in the United States in 2015, HawkEye 360 pioneered commercial RF intelligence from space. Its satellites detect and geolocate radio-frequency signals such as radar emissions, communications transmissions, and GPS interference, creating a new category of geospatial intelligence. Today, the company is a key supplier to defense and intelligence agencies.

SES O3b mPOWER

O3b Networks was founded in 2007 by satellite entrepreneur Greg Wyler to connect the "other three billion" people without reliable internet access. Acquired by SES and upgraded into the O3b mPOWER system, the constellation operates in Medium Earth Orbit (MEO) at approximately 8,000 km altitude. By balancing coverage and latency, O3b mPOWER has become a leading connectivity platform for telecom operators, cruise lines, governments, and cloud providers.

Sources: fcc.gov, SpaceX, satellitemap.space, reuters, ses.com, spacenews.com, amazon, ICEYE, AST SpaceMobile, SEC.gov, prnewswire.com. © 2026 Jarsy Research

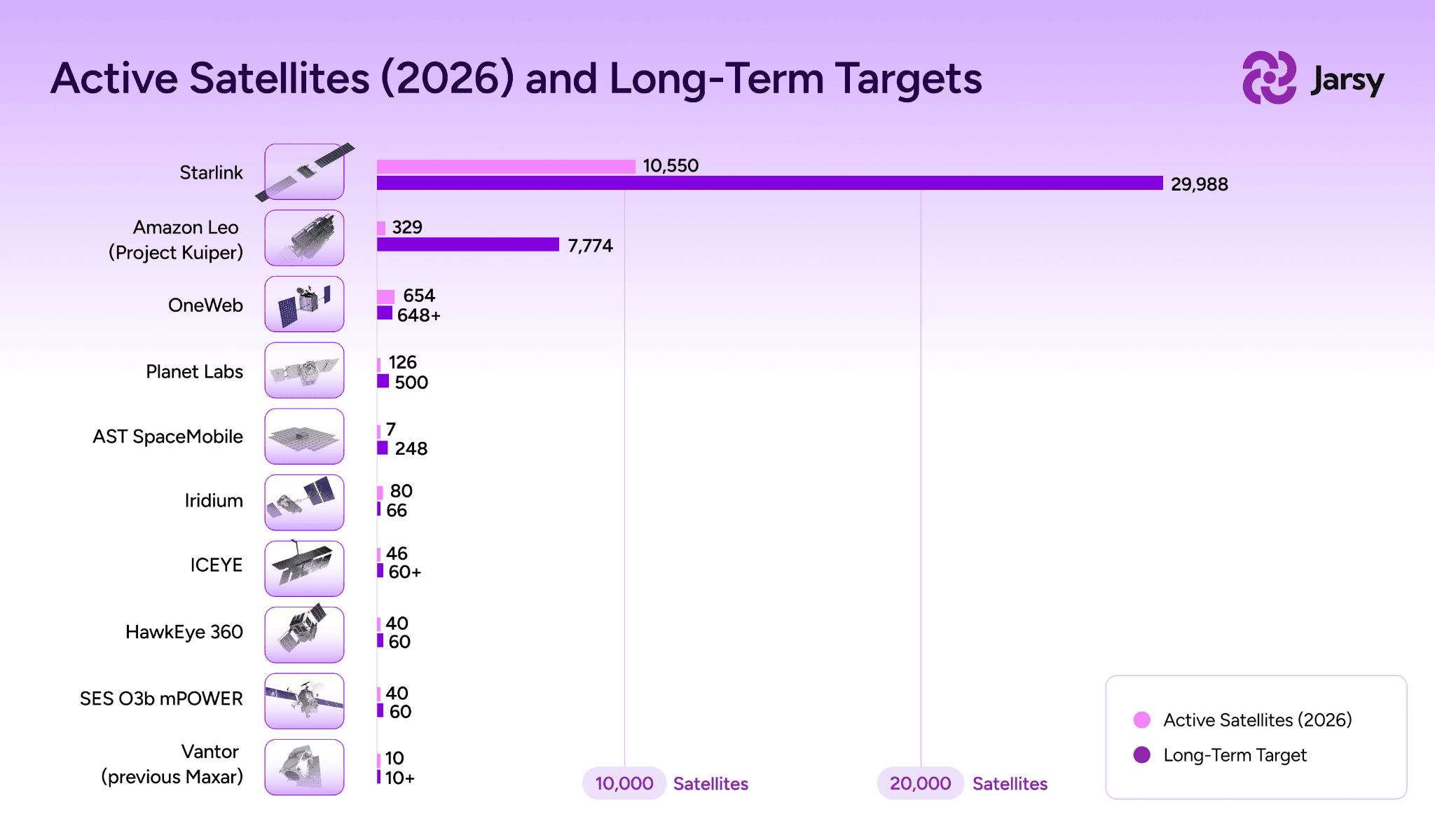

Active Satellites and Long-Term Targets by project. © 2026 Jarsy Research

6. Industry Outlook

The satellite industry is entering a new phase of growth. As discussed throughout this report, falling launch costs, satellite miniaturization, and advances in computing have transformed satellites from specialized government assets into a rapidly expanding commercial industry.

Several key trends are likely to shape the next decade:

1. Global Connectivity - Broadband constellations and direct-to-device services will make satellite connectivity an increasingly integrated part of the global communications network.

2. AI-Powered Intelligence - Earth observation companies will increasingly use AI to transform imagery, radar, and radio-frequency data into actionable intelligence rather than simply selling raw data.

3. Space-Based Computing - Advances in onboard processing and initiatives such as Google's Project Suncatcher suggest satellites may eventually evolve from communications platforms into distributed computing infrastructure.

4. New Space Infrastructure - Emerging markets including in-space manufacturing, satellite servicing, refueling, and debris removal could become important new segments of the space economy.

From Sputnik to Starlink, the history of satellites has been a story of expanding capability and falling costs. The next chapter will likely be defined by the convergence of connectivity, intelligence, AI, and new space infrastructure, further integrating space into the global economy. 📡🌐🛰️🚀📶

Further Reading: Satellite Industry Report 2025 by SIA, SpaceX 2.0: Starlink and the Era of Orbital Al by Jarsy, How to Build a Satellite by The Efficient Engineer, Planet Labs: The Operating System Anchoring a Prosperous World by Space Capital